One of the most difficult things I’ve had to overcome as an entrepreneur is dealing with inconsistent income.

One of the most difficult things I’ve had to overcome as an entrepreneur is dealing with inconsistent income.

Nothing is more frustrating than working hard the entire month and having nothing to show for it (or less than nothing) in your bank account.

It seems nearly impossible to create an accurate budget, project cash flow, and grow your business, when you can barely make ends meet.

So how can you get out of this vicious cycle, without working more hours?

Here are 5 budget tips I’ve learned since becoming my own boss for the past 2 years.

Open Separate Business and Personal Bank Accounts

This is probably one of the easiest, yet most overlooked, tips for successfully dealing with irregular income. As an entrepreneur, most of your life and work is meshed into one.

But when it comes to your personal and business finances, these things need to be separated. Not just for your sanity (although that’s enough of a reason) but also for ease of accounting and doing your taxes.

Here’s why having separate bank accounts can be so helpful:

Simplify monthly business reports. By opening a separate business account, you can use it to link your bookkeeping software, which makes creating business reports, calculating quarterly taxes, and yearly financial statements, a breeze. You won’t have to worry about excluding personal transactions from the business ones while categorizing them.

Prove income to the IRS or lender. If you’re ever audited, you can prove your business is legit much more effectively, since it’s treated like it’s own entity. You also won’t have to worry about a lender, or the IRS, sifting through your personal transactions.

Outsource bookkeeping tasks. Another advantage comes during tax time in the event you don’t have the time or resources to create year-end reports yourself, you can easily hire a bookkeeper or CPA. If your accounts are combined, you’ll either have to manually create the summaries, or let a bookkeeper sift through your personal account. That’s more time, more money, and less privacy.

Pay Yourself a Regular Salary

The key to dealing with irregular income as a business owner is to mimic a regular income schedule as much as possible. Similar to a traditional job, that pays you every Friday, or at the beginning and middle of each month, you should make frequent, and regular, transfers into your personal and business bank accounts.

Set yourself up like an employee of your business (even if you’re a sole-proprietor), for the purposes of accounting.

- Figure out your bare minimum budget. Add up all your personal expenses and necessities. Things like household bills, rent, food, and gas should be included, but make sure it’s the absolute minimum for what you can survive on. In the event you need to cut back dramatically to recover from a biz emergency, you’ll know what needs to go in order to get back on track.

- Write yourself a regular paycheck. On a set day each week, or month, write yourself a paycheck based on the budget amount. Essentially, you’re going to transfer the funds out of your business account, and into a personal one. For business expenses and taxes you’ll use the rest of the funds in your biz account.

- Prioritize your spending. The key to having a successful budget with fluctuating income is to set a reasonable salary and stick to it. Make sure your personal expenses aren’t too extravagant and that they remain consistent. Prioritize what you spend and what you’re purchasing. Try to get the biggest bang for your buck, always. This will make paying yourself a regular salary much easier.

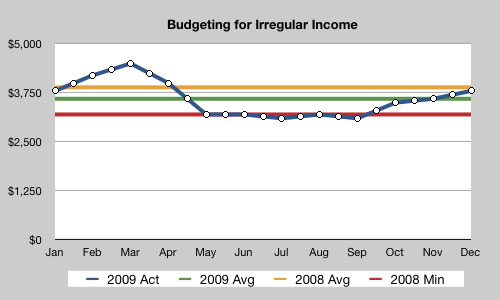

Project Cash Flow Based on Minimum Monthly Income

Take a look at the last 6-12 months of your income and expenses. What is the baseline of your income during this time period? To get a more accurate estimate, you may have to include the past 12-18 months of your cash flow.

You want to be able to project future cash flow based on your minimum monthly income from the past months (or years). Since your income varies, you should know what your baseline is and be sure you can make at least that amount.

If you notice that your cash flow baseline doesn’t cover your bare minimum budget (mentioned in tip #2), you’ll have to increase your income, or lower expenses to get back on track. Your baseline of minimum monthly income is a good measurement of how your cash flow is currently performing.

Set Aside Bonuses and Raises

This is smart tip for a regular employee, but it’s also a great strategy as an entrepreneur. When you raise your prices, land a big client, have a large month of sales, or receive a bonus, put this extra money into a separate savings account.

Don’t mix it with your regular savings goals or savings accounts, but instead use the extra funds as a cushion to tie you over in the months you have an increase in expenses (like during the holidays), or when you have less income coming in one month.

This savings buffer will allow you to still invest in your business, and make smart choices for growth, without being too stressed about where you’re going to make up the income from a slow month.

Live Off One Partner’s Income

If you have a partner or spouse you live with, try working together to live off just one of your incomes — preferably theirs if they have a traditional job with a regular paycheck. You may think this is an impossible idea, but I assure it’s not.

My friend Michelle shares exactly how her and her husband are living on one income together, with one of their main focuses to use the extra money towards debt payments. She also works a day job and runs her blogging business on the side so she can earn extra money.

Still need some convincing? Check out some of the comments from readers of Budgets Are Sexy as to the proof that living on 50% of your income is possible. The common theme? You’ll have to make a mental shift about money, and make sacrifices when necessary.

You can even join the 50% Savings Club if you want support from other go-getters who are striving to live on half their income. Living off one partner’s income isn’t easy, in fact it can be downright difficult. However, your bank account, and business, will be thankful you stuck it out.

Key Takeaways for Budgeting with Irregular Income

It’s easier to live with a budget surplus than have to make up a budget deficit, so when at all possible, stash away extra cash, bonuses, and any savings into a separate “Buffer” account.

You also have to prioritize your spending properly, create a budget and project cash flow accurately, and separate your business and personal accounts, in order to successfully navigate dealing with fluctuating income.

It’s a bit more difficult to get paid as an entrepreneur, but the added freedom and flexibility is usually worth the extra effort.

How do you deal with an irregular income? Do you have any other tips to add to this list?